The New Retirement Strategy That’s Changing the Game

May 27, 2024Are you feeling stressed and insecure about your

retirement

? If so, he is not alone. The traditional approach toretirement

planning is outdated. The old rules no longer apply, but don't worry. I'm going to share a better approach in this video. I will explain why the traditional retirement plan is no longer effective and I will also share the key steps to creating a better plan that works for you, so if you are ready to take control of your retirement and stay because I'm going to show you Hello to Everyone, I'm James Canol, founder of Root Financial and I'm here to teach you how to get the most out of life with your money.

Now I'm going to walk you through a customer case study, but before I do that. I want to summarize what I think is wrong with traditional retirement planning: The way traditional retirement planning is done is that it actually starts from a young age, you get good grades in high school so you can get into a good college, you get into a good college so you can get a good entry level position you get a good entry level position so you can work hard and move up the ranks you move up the ranks so you can buy a house start a family save for retirement You do all these things so that you can finally retire, once you get there, you can enjoy it all, but what a lot of people are discovering is that they get to this promised land, they retire, what they have been planning for their whole life and they feel that it's a bit empty, they feel like they've been sold a bit of a lie and the reality is, whether intentionally or not, in many ways they were, we've gotten into the habit of putting enough in until a future date and there's a better approach.

More Interesting Facts About,

the new retirement strategy that s changing the game...

I'm going to walk you through a customer case study to show you exactly what I mean. This is Bill and Susan's sample now Bill and Susan came to me and they've just been classic savers and they've been living retirement for terms that they went to a good college they got good grades they studied hard they got a good entry level position they did exactly what I told them they continued moving up the ranks maxing out their 401K they bought a house starting a family they did all the books Let's go over their situation to see maybe where they went wrong with this line of thinking, well here are Bill and Susan, they are both 57 years when they got to this position, we can take a look at their net worth and you can see that they have done very well now, obviously this will not apply to everyone.

Many people see this net worth at this age and this may not apply. It's okay if this situation doesn't directly apply to you, but I. I think a lot of the principles will be even if you look at these numbers and say, "Hey, that's a long way from where I am," stick around because what you'll see is that the principles are relevant to anyone as we look at Bill's situation. and Susan or your plan, you can see that the bill for your different assets has your 401k of 8 182,000. He also has a Rollover Ira, which is his previous company's 401K, about 32,21,000.

Susan has her 401K with 669,000 and then she has her Roth IRA with 76,000. They also have joint savings and joint investment checking account with around 1.2 million and then they have their housing card and a mortgage on their house. Now I'm going to repeat what I just said a second ago: Bill and Susan were classic examples of the American dream. Both came from lower middle class families. They both studied a lot. They both worked hard. They both continued saving, investing and deferring because they thought we would continue working until retirement and that's when we really are. We're going to enjoy the fruits of our labor now down the road they bought a house, they're starting a family, but there's a lot going on in their situation and I wanted to explain maybe a better way to do that or illustrate that.

Let's continue analyzing your situation. His goal was to retire at 67 years old. I asked them why and they said well, that's when Social Security says we're at full retirement age. That's what we're supposed to do according to the American dream, quote, work 40 years. then retire and be able to enjoy the fruits of our labor, so in short, even if they want to work 10 more years, today they are 57 years old, they want to retire at 67 and I will return to this point in a moment. because although it is well-intentioned to say that I want to work 10 more years because that is when full retirement age is reached, my parents worked a long time, I need to do the same, there are some wrong aspects to that, but I'll keep moving on to that for a moment , the next thing is we talk about how much they want to spend in retirement, well, you saw that they have been doing a very good job saving.

He said we've been saving for a while, at least we do. We want to enjoy this a little, so we're going to spend $12,500 a month in retirement, which is $150k a year after taxes. On top of that, we're projecting healthcare expenses beyond these basic living expenses, but those are the expenses and the goals that they had in retirement the next thing we're going to look at is their income, like I said, they worked good jobs, they had good jobs, they moved up the ranks, Bill now makes 220,000 a year, Susan makes $240,000, $45,000 a year and then when they retire they will both have their social security benefits which will be strong healthy benefits based on their history of income.

In fact, if we want to dig into them, the Social Security Bill is projected to be 3,400 per month and Susan's benefit is projected to be the same, so both strong benefits the next thing we look at is savings, so they are deferring much of their income through the 401K, so they are both saving $30,000 per year in their 401. The UC bill is getting a 3% match on their contributions. and Susan is also getting a 3% match on hers, so they are each saving $30k, her employers are putting in another 3% and they are also saving $2,000 a month in their joint investment account.

The next thing we looked at was their investments, so we know how much they have in 401k and Roth IRAs and joint accounts, but we need to be able to project some rate of growth, some rate of return on those assets in the future. That's where we got here, we said based on your mix of US stocks. International actions. emerging markets, etc., this wasn't necessarily our recommended mix, that's how your portfolio was allocated. Their return we project will be around 8% and we will reduce it to 65% per year after they retire, assuming that they will be invested a little more conservatively at that time, but this was an initial rate of return that we are going to assume that this is the first place I wanted to go with Bill and Susan, now we understand their goals, where they are with their current assets what their sources of income are now and in the future with Social Security we understand what rate of return we are going to project.

Now let's make a projection of what your retirement would be like. Well, to start, we need to understand what your retirement will be like. your portfolio will be retired, well if your portfolio balance today is about $3.2 million, you are both saving 30 grand per year in your 401k, so that's 60,000 total, your contribution is another 14 of the grand combined 6,600 for employer bills 7,350 for Susan's employer, so when you add up her 401K Contributions plus matching contributions plus the 2,000 per month or 24,000 per year to her joint account plus, if we assume a rate of return of 8%, your portfolio is projected to grow by more than $250,000 this year the final balance of your portfolio at the end. of the year there are 3.6 million.

A word of advice: this is never guaranteed and we know it, but for the sake of projection we should assume some growth rate, even if they get 8% a year for the next 10 years, it's not going to happen. being 8% every year will never happen that way some years it will be much higher, others much lower, they may not even get 8% in the next 10 years so it's okay the point is just to have a point starting to be able to project to see what this would look like under these assumptions, but then of course we can always challenge and adjust these assumptions as we go, but this is what I showed you.

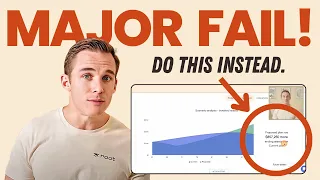

I said Bill Susan, this is where you are today. You've already done an excellent job. saving, but look what the next 10 years will do yes, it took you about 35 years to get to your first 3.2 million. What will the next 10 years be like? Well, if we do this every year for the next 10 years. By the time you retire, it is projected that you will have almost $9 million in your portfolio, so over the next 10 years the compounding will really start to take hold, where your portfolio, which earns 8% annually on average, is growing by half a million. dollars per year in many of these years, so that's what I'm projected to have at retirement, and as we look at this, it looks like so far so good, not bad to have $9 million in my portfolio at retirement. excluding real estate and I also know that I have other sources of income like Social Security that I will be able to rely on.

I don't see the problem so far, so we went ahead and the next thing I showed them was we projected what their income will flow into in retirement, so social security for each of them will start at age 67 and how does that compare? with your expenses? Well, their basic living expenses would be $50,000 per year, adjusted for inflation, by the time they retire. The inflation-adjusted equivalent of 150 thousand dollars today would be a little more than $200,000. On top of that, they would still have a mortgage payment for at least the first two years of retirement and would pay it off early in the third year, so we will be projecting the health care beyond that, yes, they have Medicare, but they still have Medicare Part B premiums, Medicare Part D premiums, and then they assumed out-of-pocket expenses beyond that, so we set their expenses and assumed a projected tax rate for your total expenses. they're closer to $33,000, so I said Bill Susan, here's how we read this graph, you have $95,000 of income and that will go up a little bit as we go as Social Security gets some cost of living adjustments, but here are your expenses. more than $300,000 and are expected to increase so that the net flows this is what your portfolio must be able to generate so that you can supplement Social Security so that you can pay taxes you can pay your healthcare expenses you can pay your mortgage and then You'll have the equivalent of $1.15 grand per year left over so you can live and do everything you want to do.

The last thing we want to do with this is understand what this represents as a withdrawal rate. This is a lot, if you've seen any of these case study videos, to me this number is irrelevant it's $227,000 well, well, it depends. I'm telling you that if you have $200,000 in your portfolio, this is a really bad number, it means that you are going to deplete your savings in a year if you have $10 million in your portfolio, although this is only a 2% withdrawal rate, so We need to compare this withdrawal to the actual balance in your portfolio to get what this represents as a withdrawal rate, so here is what that page looks like when we compare the dollar amount they are taking from your portfolio to the value of your portfolio. , your withdrawal rate starts at 2.3%, but then your mortgage pays off and drops even lower than the averages, not until required distributions begin at age 75, raising your withdrawal rate even by above 2.5 percent. so again, it looks pretty good, these are very sustainable numbers.

They were starting to wonder why I was worried about their plan before they got into my worry about their plan. The last page I showed you was this one. I said Bill and Susan, this is where you are today with your portfolio balance this is what it's projected to look like when you retire, so as we talked about, you have about $9 million in your portfolio. His portfolio is projected to continue to grow so much that he is projected to spend around $23 million in his portfolio by the way that doesn't even include the value of his house, if we include the value of his house he is closer to a net worth of $28.3 million at that time, this is my concern, my concern is not your finances your finances are in a very healthy position and it was not like this by chance, they became like this because of your hard work, they became like this because you started to save and invest early, they became that way because you have been extremely diligent in living within your means and prioritizing saving and prioritizing planning for the future, there is a wonderful book called Dying with Zero by Bill Perkins and in that book Bill Perkins has a quote that I think is extremely relatable to what my real concern was with this. situation I'm going to read you that quote that says: I suppose your goal in life is not to maximize your income and wealth, but to maximize the satisfaction of your life, which comes from experiences and the lasting memories of those experiences.

Let's bring that back to Bill and Susan, if I go back to their plan, look at how much they are projected to have in their portfolio, which alsoThey shared with me, although as we go through this process, yes, we have high paying jobs, yes, we are saving. a lot, but we can't really enjoy this much, our job is incredibly demanding, we can work 60-70 hours a week and sure we have high portfolio balances, but what's the point of that if we can't even fully enjoy it? So, in a way, they have been looking forward to retirement, but at the same time they continue to push that age back, never trying to understand whether we could retire earlier.

Could we spend more today? Could we do more of what we are not planning? I've just been in that traditional retirement dream mentality of save save save defer defer toer and once we turn 67 we will have enough money to do whatever we want or that's what we think, this is what we need to understand, we all have three resources that we must have We very intentionally balance those resources: our time, our health and our wealth, and normally what we do is sacrifice our time and our health to obtain more wealth. The Bill and Susan example, that's exactly what they were doing, but they didn't do it.

They didn't have time because they spent everything at work and another thing they had slept on was their health. Their health had been affected because they spent so many hours at work that they couldn't do the things they liked to do. They couldn't stay active. They didn't go to the gym or They were staying healthy like they used to and that had been an important part of their life, so when I took them back to this graph that I shared with them, I said, look if we're trying to balance those three resources your time your wealth and your health I'm not worried about your wealth look at this wealth right here even if inflation is higher than we think it will be even if taxes are higher than we think they will be you' We're still in a position where we have a lot of room to be well and we started having that conversation where we said, Are we sacrificing too much of our time?

Are we sacrificing too much of our health just to be able to get into this position to retire? with more money than we will ever be able to spend in our lifetime, so we talked about it and one of the difficult things is that this is a difficult concept to adopt and accept from the beginning, so Bill started it to have a little pushback He said, well, isn't that okay? You know, at 67 we will have more than enough money to do whatever we want. You know, we can make up for lost time again and again. a conversation about that and going back to the book dying with zero Bill Perkins says this which I think is a wonderful quote and it really relates to this comment that Bill and Susan made in the book Bill Perkins says that our culture's focus on work is Like a seductive drug, it takes all your longing for discovery, wonder and experience promising to give you the means, money to achieve all those things, but the focus on work and money becomes so single-minded and automatic that you forget what you are doing. you were longing for.

First of all, that's what I talked to Bill and Susan about. Next, yes, on paper, that is absolutely true. You will be able to make up for lost time. Here you have all the money to do the things you want to do, but. The reality is that when you get here, if you are not intentional about your health, if you are not intentional about the experiences that you enjoy, if you are not intentional about the activities and things that really give you life, they will not. We're going to magically appear on the day you turn 67 and retire when a lot of people get there.

We have been defeated by so many years of work, mortgages, family and things that are simply wonderful, but they take their toll. us and if we don't prioritize those things that really give us life, they won't magically appear now before we continue here. I want to take a second to say what I'm not saying. saying work is bad I'm not saying you should leave work as soon as you can I'm not saying work isn't part of a well-balanced life work is amazing I love work I think a lot of people love work the problem It's when we put everything we have into work thinking that it will somehow get us to the promised land of more freedom more money more time we are missing the point what is the point of doing all that if we are missing out? the experiences, time, and things that bring us joy and purpose along the way, so there's a part missing from most people's thinking that simply says: Hey, more money means more freedom, but only in the as long as you understand what it means. that freedom even seems like what brings me Freedom, what brings me joy, what brings me purpose and ideally we integrate those things along the way instead of postponing them until some vague and uncertain date, so the real problem is that Too often work becomes a very socially acceptable form of distraction and it distracts us from asking ourselves who we really are, what do I really enjoy, and instead of asking those really difficult questions, we ask what I think sometimes is the easiest job to put in more hours, work more days, work more years. save more, dilute ourselves in the thought that that will somehow unlock freedom in the future, but if it doesn't unlock freedom today, it probably won't in the future either, so back to Bill and Susan, what did I give them or what I told them?

They based themselves on this plan that on paper looks incredible. The first thing I started asking them was: Bill Susan, do you love what you do for work? You know, because there's one thing that if you really love what you do for work, you don't do it. stop doing that, make sure it doesn't interfere with other things that are important to you, but I did my research, tell me about the job, they didn't really love it, now they were doing it out of a sense of duty, hey, we've put so many in. years, hours and studies to get to where we are, it feels strange not to continue working like this.

You know, our income is at a place where it feels like Weir isn't doing this anymore, but no, James, we don't really love it. The other thing. They told me look, we're working so much, you know, it's 50 or more than 60 hours a week that we can only take the weekends to recharge briefly and then we come back and do it all over again, so not only do we not love what we we make. We do it for work, but we don't even feel like we can live fully outside of work because work has become so demanding.

The next thing I did, like I said, tell me more about your desire to work until you're 67, so you're 57. today why 67 where does that number come from and they said James well to tell you the truth that number seems easy because that's when the Insurance Social tells us that we are at our full retirement age and on top of that, as we mentioned, we both came from lower middle class families, you know, our families didn't have much, our parents worked until they were 70 because they had to, so For us we almost feel this feeling of guilt for not continuing to work like our parents did before us.

I said okay and lastly I want you to tell me about the spending, you know, 12,500, it's certainly a healthy number, it's a lot more than the average person spends in retirement, but at the same time you have a lot more in your portfolio than the average person does when they retire, could they spend more? And they said, James, yeah, we'd love to be able to spend more. We can easily find things to spend money on. You know, maybe when we travel we pay for our children and grandchildren to come with us. all expenses paid there are plenty of charities we want to support, spending more could simply be donating more to charities so yes James we absolutely could, we've always felt a bit guilty about saying we want to spend more than this amount.

So that's where I said Bill Susan, that's wonderful feedback. Now let's go back to your plan for a second. That's how I see things. You're in a position where, because of your hard work, your savings, and your investments, you're projected to have a lot of money left at age 90, but what traditional retirement planning gets wrong is that it tells you to postpone everything. what you want to do up to this point only to say that you have millions of dollars left over that you will never make. you can enjoy now that 23 million may be more, maybe less by the time you get there, but let's look at some options.

The first thing you told me is that you don't love your jobs today, but you used to enjoy them and You used to enjoy them, but you got promoted to management positions, so you like the work you do, but you don't like them because you got promoted and now you're in management positions. those who are not doing the job you want. they're managing others who are doing the work, so I just suggested what would happen if they demoted themselves and if they came back to work and said look, I want to be in this role where I can do the work but I don't want to have the responsibility. of managing people, James, we could do that, but it would come with a pretty serious pay cut and I said, okay, let's look at this, what if we went back to your plan and said, instead of maxing out 401k, what if would do the same? minimum here just to get the match Bill, what if you adjusted your contributions and really this is closer to 6,000 each?

What would happen if you stopped saving in your joint account completely so you could accept a lower income because now you're going to save less than that? income, so while you would accept downgrades, your actual cash flow for the things you'd like to spend money on hasn't changed at all, what would that look like in this scenario, well, we re-ran the numbers and, as we saw it, yes, it means they have fewer dollars in their plan at the end of the day, but they are still projected to have almost $19 million, but I asked them, I said, Bill Susan, what would happen if they were downgraded, what would that mean for the style of life?

They looked at each other and said Well, it would be great for the first lifestyle: we would enjoy the time we spend in the office each week, which is a lot, but second, we would have a lot more time out of the office and we could easily leave our work at home. We could more easily go see a movie on a Tuesday night, go with friends to dinner on a Thursday night, and not have to worry about rushing home to prepare for tomorrow's meeting, so when we start talking about this, We said how much it would improve their quality of life.

Improve today if you cut your salary a little by taking steps that actually allow you to do work that is more meaningful and enjoyable for you. I took this one step further. I said, look, today you are 57 years old and you want to retire at 67. The next 10 years could be the best 10 years in terms of health and energy that you are going to have. Do you really want to continue working in a job where you can't fully enjoy the health and energy you have? because you're giving everything to your employer and it's not really necessary when we look at your financial projections, they thought about it that way, they felt like they were getting 10 years of their life back, they say, James, you mean to tell us that we?

We can enjoy what we do at work for the next 10 years instead of fearing it, it means we can spend more time with friends and family during those 10 years, it means we can prioritize our relationship better during those 10 years and we just it's going to cost a small percentage of our total net worth by the time we're absolutely over and all of a sudden this started looking very attractive and then just to show you some other options, Bill Susan What If said instead of downgrading it. You yourself may not make that option, but what if instead of working until age 67?

What happens if we cut that time in half? What happens if you don't work until you're 67, but it's 62 years, so instead of working 10 more years, you work five? More years, what impact will that have? It's pretty significant if you just look at this number, maybe there's $10 million less left at the end of the day, but you're still in a great position where you're projected to have a healthy portfolio balance. at the end of your life, but think again about what those 5 years could do in terms of your relationship and the time you have to enjoy each other's company.

What might that do in terms of your ability to be with your growing children? since maybe they're moving to different places around the country and starting their own families, what would that look like in terms of the trips they can take, the activities they can experience, the things they can experience? If we could get you off work sooner again, I'm not saying work is bad for everyone, but it was stressful for them, and it wasn't completely necessary. So the last thing I said to them was: could you spend? over 122,500 a month if I wanted to and they said sure but it would probably be in the form of charitable donations or maybe even helping our kids with down payments on their houses or whatever it takes so let's explore that because like from now on Going forward, you might have $23 million to give away when you die, but that won't be for 40 years, 35, 40 years or so, it's a lot.time to wait for that money to do the good you want it to do, let's see what it is.

What would it look like if you wanted to make an additional $225,000 in charitable giving each year? What would that look like? Well, if we look at this, what that means is that yes, that's $1.3 million less that you have at the end of the day, but if this is going to be a charity or part of a charity anyway, that money is will get to work sooner. They also said that we would love to help the children. You know, we would love for them to stay in Dallas, where we are, and be able to shop. a house near us if we want to keep the family close, but they may be priced out, things are getting very expensive, so I said what if you could help each child with a down payment?

We're talking about $75,000 each. They have three children. Do that. for three years we gave away $75,000 when we started running these things, it barely made a dent in our long term projections, we didn't give to everyone, in fact most people are not where Bill and Susan were in terms of their finances, but These principles apply to ancient tradition. thinking is saving saving saving putting off putting off turning 65 or turning 70 and then enjoying it, you know, most people don't realize that they're probably on their way to having more money than they could ever spend in their lifetime, rather than how can we start doing things today in terms of finding more balance with work in terms of working fewer years before we can do the things we want to do in terms of giving more or spending more the goal of planning is not die with the most money but live more aligned life, traditional thinking about retirement is wrong and then prioritize one way to maximize your butts for retirement and then you can have a good time, that's not the way most of people want to do it when they realize there is a better way and that better way. it can start today, that's where the transformation happens of understanding that this money can be used for a much better good than just sitting in my wallet, so when I'm 90 or 95 I end up passing away and then I do something different.

What are the conclusions here? What is the new line of thinking I encourage most people to think about? Well, number one is that this specific example doesn't apply to everyone, but what I do see is people who are frugal throughout their lives and people who prioritize saving and investing often fall into this routine where they don't They can't spend, they can't retire early, they can't really enjoy any of this and what they end up realizing is that they did it all. They sacrificed so much that they crushed some of the things they would have enjoyed along the way and why didn't they enjoy it anyway when they retired, so how could they have a more balanced approach?

The second conclusion is intentional money is not the goal, money is the tool, that money at the end of your life is not going to do anything for you if you say well James, I'm going to give it away or I'm going to give it to wonderful children. Can you start doing it earlier? Can you start doing it when there is more need both with charity and maybe even with your children? How can you use that money in a more aligned way today instead of just using it and deferring it forever because having a bigger wallet when you're dead is not the real goal use that money as a tool to help you discover and help you achieve the things that are really important to you the third conclusion is to see life in a more comprehensive way, do not see it as pre-retirement and post-retirement and pre-retirement and pre-retirement means save save save save save save post-retirement means now I can enjoy it enjoy today yes plan for the future because It absolutely may be too unbalanced in the other direction too, but looking at life more holistically, where can I spend more today?

Spending more today would impact my future goals, if not how can we reimagine the way we work, the way we spend, the way we save and view life more holistically instead of just pre-retirement and post-retirement and then the fourth conclusion, the final conclusion and I'll be honest, this is probably the hardest one, this is where the real work begins once I showed Bill and Susan that they could stop working earlier, that they could spend more today. Becoming financially independent before you thought you could, that's where the real work is. They didn't realize this, but after years of work and sacrifice and giving so much of what they had to their companies, they almost forgot who they were, yes, we belong to each other.

Spouses first and foremost and then parents after that, but who are you beyond that? who you want to be what things are important to you what makes you fully alive those are difficult questions that most people don't consider it's time to answer because they just think that magically those things will appear to them if they save enough money for when they retire , so this is the new way to no longer sacrifice your health in your time in your zeal just in pursuit of a greater portfolio balance at some point in the future, now it is about understanding that money is a tool and that The options available to you if you plan correctly and effectively become limitless, so how can you take that perspective into your planning to ensure that you are using your money as a tool to live an aligned life rather than looking at your money as the goal. in itself, so as you look at this and say, well, this is great, but how do I know when I'm on Bill and who's in this position, how do I know when I've had enough?

I'm going to put a video on the next screen that talks about that and will help you understand when I know I have enough to be able to start doing it. some of these things and live more intentionally instead of just continuing to save and invest forever once again. I'm James Canol, founder of Root Financial, and if he's interested in seeing how we help our Root Financial clients get the most out of life. with your money be sure to visit us at www.ro Financial partners.com

If you have any copyright issue, please Contact