Prepare A Cash Flow Statement | Indirect Method

Jun 06, 2021In this video you will learn how to

prepare

acash

flow

statement

using theindirect

method

. I'll show you how thismethod

is different using the direct method, what it looks like, and how to calculate all the numbers using an example. Hello viewers. I'm James and welcome to another accounting staff episode. If you're new here, this is the channel where we post weekly videos teaching the basics of accounting. If that's something that might interest you, you get the subscribe button so you don't miss this video. We are going to cover preparing acash

flow

statement

using theindirect

method.

I've already done a couple of videos on the direct method where I explained the format and purpose of the cash flow statement and how to

prepare

it using the T-accounts link here if you missed any of these this week, we'll use the same income statement example and balance sheet that we used last time, but we will prepare it using the indirect method. I recommend that you watch this video until the end. because I'm going to walk you through all the calculations step by step so you won't have any problems putting one of these together yourself, so without further ado let's get started, what's the difference between the direct and indirect method anyway?

More Interesting Facts About,

prepare a cash flow statement indirect method...

The cash flow statement, along with the income statement and balance sheet, form the three main financial statements. We use the cash flow statement to summarize the movement of the cash balance on a balance sheet over a period of time, usually a quarter or a year, and we do this by summarizing all cash inflows and outflows into three cash flow categories. operating activities cash flow from investing activities and cash flow from financing activities the last two sessions cash flow from investing and financing activities are completely identical whether the direct method or indirect method is used the only section that is different is cash flow from operating activities, so I want to focus on that section in this video.

If you want to learn more about investing in financial activities, I have covered them in more detail in the previous section. Two videos that I will link to in the description. Operating activities are the main revenue-generating activities of a company. These are the transactions that occur on a regular basis. In the correct method, there are three steps to calculate cash flow. operational activities and I will explain it right now. First of all, we need the company's net profit or loss that we can find in the income statement. This method relies on starting with net profit and adjusting it again for non-cash transactions.

Again until we are left with just net cash inflows or outflows, most large company accounts use the accrual basis, meaning that their profits are not equal to their net cash inflows on an accrual basis. Revenue is recognized when earned, not when cash is received, and expenses are recorded when incurred, not when cash is paid, so revenue does not equal cash receipts and expenses do not equal cash. cash outflows, which brings us to the second section, we need to add back all the non-cash expenses that exist in The normally non-cash profit and loss items relate to things like amortization of depreciation or profit or loss on disposal of non-current assets.

These do not represent cash outflows, but are deducted on our income statement when that net profit is reached, so it stands to reason that we need to add them back to eliminate them from our calculation. The third and final step is that we must adjust the movement of working capital. Working capital is simply current assets minus current liabilities. Current assets are generally made up of inventory and accounts receivable, while current liabilities are made up of accounts payable. To determine whether it is necessary to add or subtract these movements in the calculation, it is necessary to consider the impact they have on the cash balance.

An increase in inventory means that the company has less cash because it has purchased more inventory than it is selling and, on the other hand, a decrease in inventory means that a company has more cash because it has sold more inventory than it has purchased. The situation with accounts receivable is very similar because they are also assets. An increase in accounts receivable means you have less cash. has been recovered from customers, so the cash balance and a decrease in accounts receivable means that more cash has been collected, so the cash balance increases, on the other hand, accounts payable is a liability , so they work opposite to inventory and accounts receivable, an increase at Pebbles means more cash because less has been paid to suppliers to whom the company owes money and lower accounts payable means less cash because it has been used more to pay the bills.

Cash flows from non-current assets and liabilities tend not to be included in cash flow. from operating activities because they are normally classified into the other two sections: cash flows from investing activities and cash flows from financing activities now that we have well worked out the basic calculation for cash flow from operating activities that is practiced using this template with a worked example, we will continue with the Chudley canon example that I showed you in the previous two videos last time I showed you how to calculate cash flow from operating activities using the direct method and today I will show you how to do it using Instead , I'm starting right now with the indirect method.

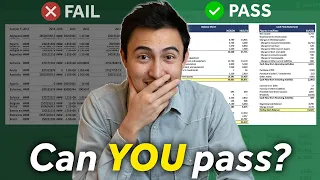

Step One: First we need to write down the net profit figure because this is our starting point that we will make adjustments to to arrive at that net cash flow. The net profit can be easily found at the bottom of the income statement, in this case Canons has made a net profit of $70,000 for the year, so we note this at the top of the calculation. Then we have step two, this is where we need to add back up all the non-cash expenses shown on the income statement. We have to reverse them from our net profit to get closer to the cash flow figure.

To do this, we review the income statement and look for any depreciation, amortization, or gain or loss. On the non-current asset disposition, in this case we can only see a depreciation of $23,000, so we need to add 23 back to our calculation to adjust for the depreciation. Finally, in step three, we must adjust for the movement in working capital, as I said before. Made up of current assets minus current liabilities, let's take a look at the balance sheet and see what current assets we have. I can see cash receivables and planned inventory. Team popteen is an acid that affects cash flow from investment activities, so we can ignore it. that and cash is what we're reconciling to on the cash flow statement, so we can ignore that one as well.

We are left with only inventory and accounts receivable. An ending inventory balance of 94 minus the beginning balance of 68 gives us an increase. in inventory of 26, increases in inventory are represented as deductions in the calculation of cash flow from operating activities because the company has spent cash purchasing raw products or manufacturing them, so we enter negative 26 in our calculation. Now let's look at the accounts receivable here we have. an ending balance of one hundred and twenty and a beginning balance of ninety-eight, which gives us an increase of twenty. Over the course of the year, increases in accounts receivable must be deducted from our net profit when calculating cash flow from operating activities because higher accounts receivable means that the company has recovered less cash from its customers, so we enter negative 22 in our Calchas, that is the movement in our current assets, but we also need to link the movement in our current liabilities so that we have considered all of them. of working capital Reviewing the balance sheet once again shows us that our current liabilities are made up of accounts payable salaries payable interest payable and income tax payable long-term loans are suggested by their name our non-current liabilities which are They relate to cash flow from financing activities, so we can ignore them here where equity and retained earnings relate to equity, so they can also be excluded.

We are left with only these four current liabilities, the sum of their ending balances is one hundred and fifty-six and the sum of their beginning balances. The balances are one hundred and thirty-one. When we take the difference between these numbers, we have an increase in accounts payable of $25,000 over the year. Increases in accounts payable must be added to our net profit in order to calculate cash flow. That makes sense, because you can imagine. that if a company doesn't pay our bills then they keep your cash, so we add 25 back to our operating boom, those steps one, two, three are complete, all we have to do now is take the total of those numbers and We were left with a net cash inflow from operating activities of $70,000, which wasn't so bad if we arrived at this number using the indirect method, but a quick review of our calculations using the direct method shows that we also we reached seventy. thousands of dollars of cash inflow from operating activities we get exactly the same answer using either technique, so which is better?

If you've seen my other videos on the direct method, you'll notice that the indirect method is much faster, which is why most large companies that use the accrual basis of accounting tend to calculate their cash flow. this way, but if that's the case, why doesn't everyone do this? I guess it really comes down to how the cash flow of operating activities is presented in the cash flow. Statement Layouts using the direct method are much more intuitive to read because they reflect the cash income statement. We have cash receipts from customers at the top and below we have cash paid to all the various suppliers and stakeholders that you make. easy reading for investors who might be taking a look at the cash flow statement to extract meaningful information from it;

On the other hand, the design of the cash flow of operating activities under the indirect method is much less intuitive; You can think of the indirect method as a shortcut to calculating cash flow from operating activities, which is an advantage for the accountant or bookkeeper who prepares it because it saves them time; However, third parties who view the finished cash flow statement lose out as this report is not as useful to them as I am. As we mentioned earlier, in this video we omit cash flow from investing and financing activities because these sections are identical in the direct method.

If you want to learn more about them or the cash flow statement, I recommend you check out the other two videos I linked below, thanks for watching, we have new videos every Monday here on things about counting, if you found that helpful , like, share, comment, subscribe if you haven't already, good luck with those cash flow statements. This is an area. which a lot of people struggle with, but I promise you that if you follow the steps I just showed you, you will be fine, see you next time.

If you have any copyright issue, please Contact